Hello there!

Need Help? We are right here!

Need Help? We are right here!

Search Results:

×

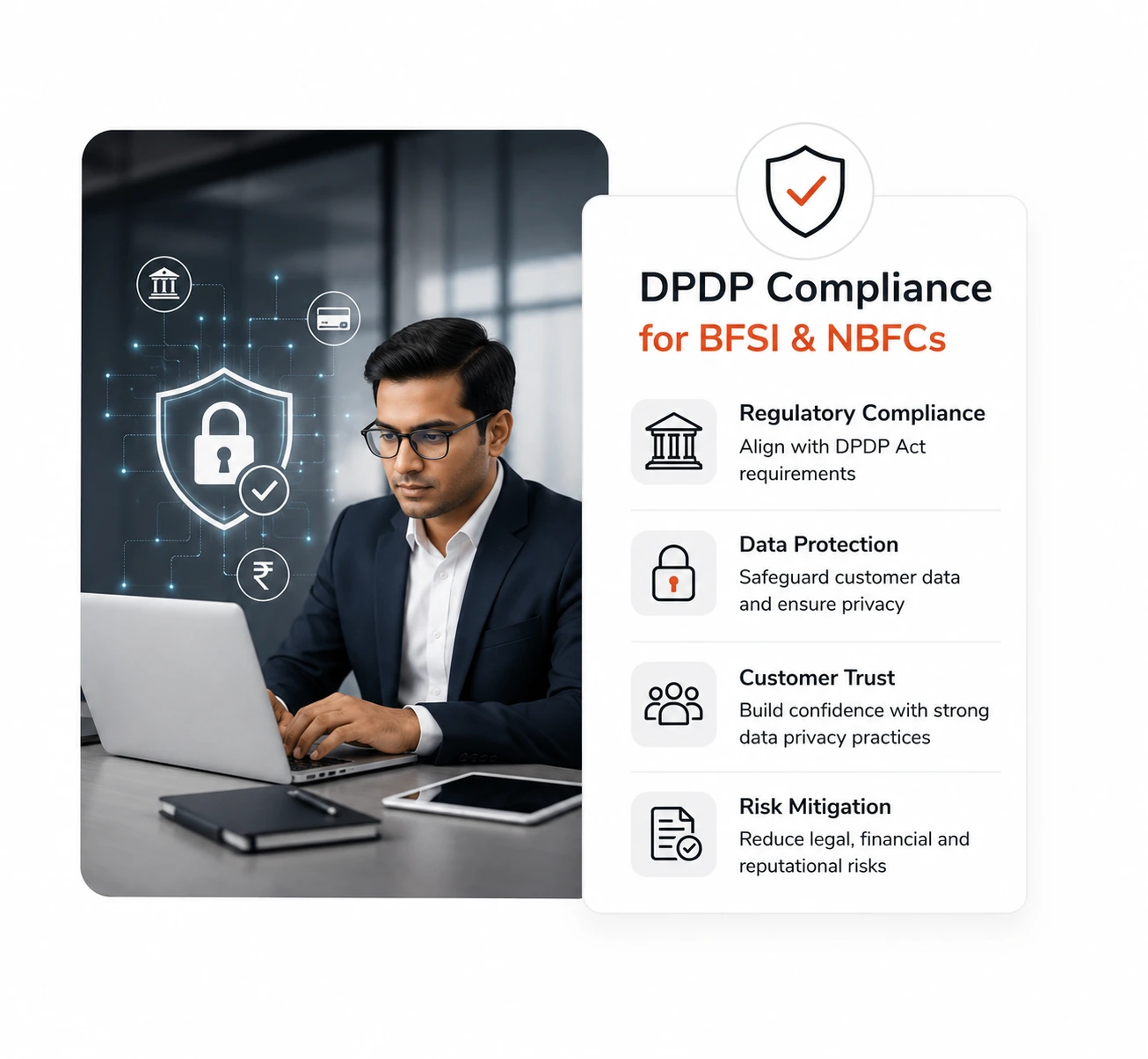

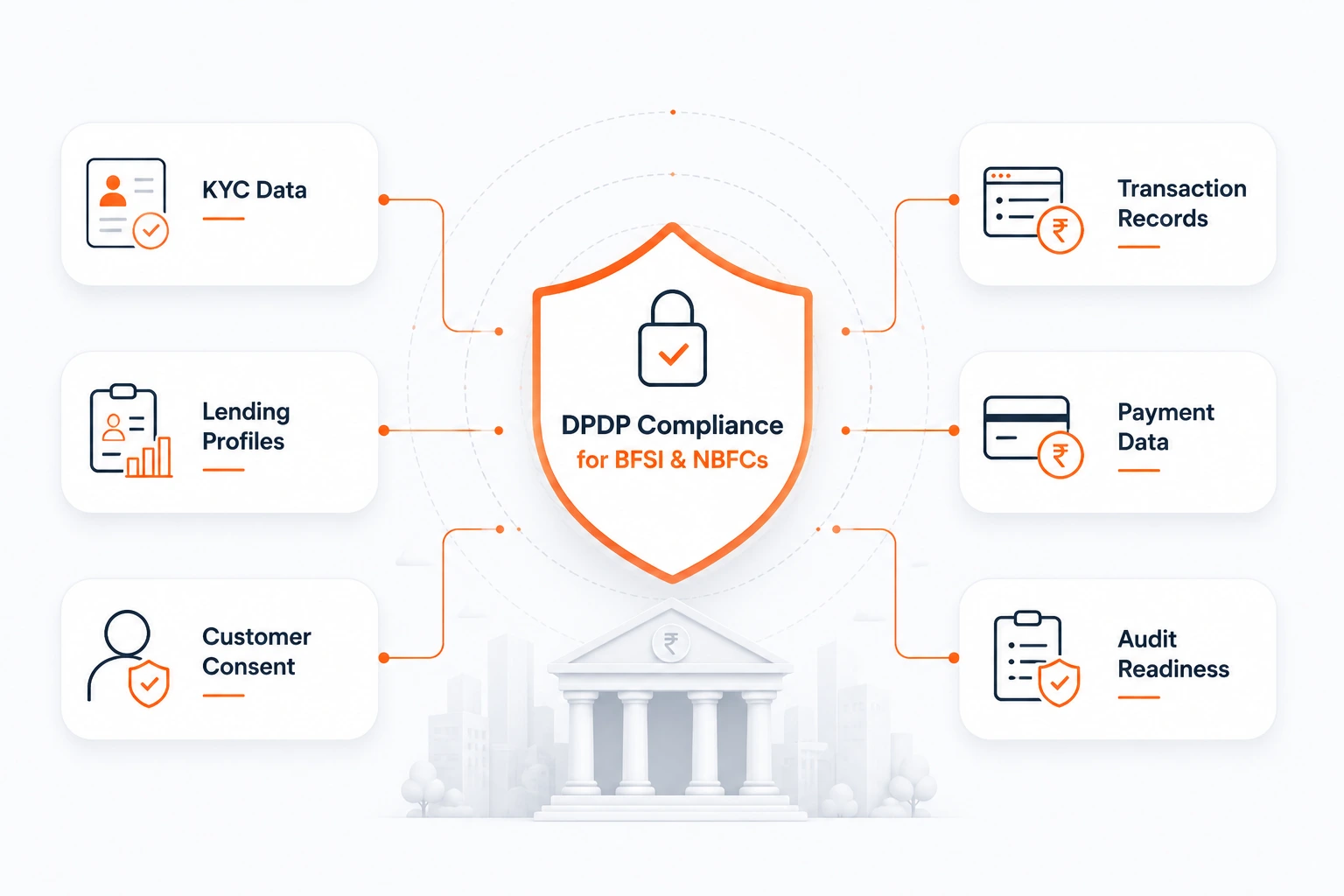

Financial institutions operate in highly regulated environments, handling KYC data, transaction records, lending profiles, payment data, and behavioral insights at scale. The Digital Personal Data Protection Act, 2023, introduces clear requirements for notice, consent, purpose limitation, and accountability across how this data is collected, processed, and shared.

Achieving DPDP compliance for banks requires more than documented policies. Banks, NBFCs, and financial institutions must operationalize privacy controls across digital lending platforms, fintech integrations, and third-party ecosystems. miniOrange enables this through a unified customer consent management platform and Privacy-as-a-Service, helping organizations enforce user rights, govern data flows, and maintain audit-ready compliance across systems.

To operationalize DPDP compliance, BFSI and NBFC organizations need structured capabilities that enforce consent, govern data usage, and demonstrate accountability across complex environments.

Capture explicit, purpose-specific consent across KYC, lending, transactions, and analytics. Maintain version history and enforce real-time consent validation across applications, APIs, and third-party integrations.

Provide customers with a centralized interface to manage consent, update preferences, and exercise rights, including access, correction, and erasure, across digital banking and fintech channels.

Deliver clear data collection notices that define what data is collected, why it is used, and how long it is retained. Enforce purpose limitation across all processing activities.

Define and enforce retention policies aligned with regulatory and business requirements. Automate deletion workflows and ensure timely handling of user-initiated erasure requests.

Identify and map personal data across core banking systems, NBFC platforms, CRMs, and analytics tools. Enable classification to support purpose limitation and efficient response to user requests.

Support compliance with governance frameworks, internal audits, and DPO responsibilities. Enable DPIAs, policy management, and ongoing compliance monitoring for regulated financial entities.

Manage consent across KYC onboarding, transactions, and account services. Ensure transparent data usage, enforce purpose limitation, and maintain audit-ready compliance across channels.

Enable digital lending app compliance by capturing explicit consent for device data, credit scoring, and third-party integrations. Govern data flows across APIs and lending ecosystems.

Handle policyholder and claims data with structured consent and clear purpose mapping. Enable user rights workflows and ensure compliant data sharing across underwriting and claims processes.

Manage consent across payments, wallets, and embedded finance systems. Ensure compliant data sharing with partners and maintain visibility across APIs and third-party services.

Manage consent, user rights, and data access from a centralized platform aligned with DPDP compliance for banks, NBFCs, and fintech organizations.

Support high-volume transactions, sensitive financial data, and API-driven ecosystems with structured controls aligned with RBI data privacy compliance expectations.

Extend beyond technology with onboarding, policy design, DPIA support, DPO advisory, and continuous compliance monitoring tailored for financial institutions.

Implement enforceable consent, centralized governance, and continuous monitoring across banking platforms, NBFC systems, and partner ecosystems.

Download Datasheet

Get the clarity you need before you commit.

x

Your download should start now. If not, please email us at dataprivacy@miniorange.com or contact us.

Please enter your work email-id